Context: The houselisting phase will be conducted in each State over a 30-day period; second phase of the count will be carried out in February 2027.

The first phase of Census 2027, the houselisting operations (HLO) phase, will be conducted from April 1 to September 30 across all States and Union Territories, the Registrar-General and Census Commissioner of India said in a notification.

This phase will be conducted in each State over a 30-day period, with the specific dates to be notified by the States.

The self-enumeration option will be available 15 days before the start of the phase.

“The houselisting operations of the Census of India 2027 shall take place between 1st April, 2026 and 30th September, 2026 in all States and Union territories in India during the period of thirty days specified by each State and Union territory. There shall also be an option for self enumeration which shall be conducted in fifteen days’ time period just before the start of house to house houselisting operations of thirty days,” Census Commissioner Mritunjay Kumar Narayan said in a Gazette notification.

This will be the first digital Census and the first to enumerate caste in Independent India.

Household queries

The second phase of the Census is the population enumeration phase in February 2027.

Caste identities will be enumerated during this phase.

The pre-test or the preparatory exercise for the first phase of the Census was held from November 10 to 30 last year in select areas across the country. It had sought household responses to 35 questions, including the composition of the floor and roof of the house, main cereal consumed, source of drinking water and cooking fuel, and the number of married couples in the house.

About 30 lakh field functionaries — including enumerators, supervisors, master trainers, charge officers, and Principal/District Census Officers — will be deployed for data collection, and supervision of Census operations.

The Agriculture Ministry released the draft Pesticides Management Bill, 2025, seeking public comments on the legislation that aims at replacing the 57-year-old Insecticides Act, 1968, and the Insecticides Rules, 1971, with enhanced penalties for violations.

The Ministry has invited feedback from all stakeholders by February 4, 2026, to refine the legislation before it is introduced in Parliament.

The proposed farmer-centric legislation introduces several reform measures.

The Bill incorporates digital methods and technology to streamline processes while imposing stricter controls on spurious pesticides through higher penalties.

Key features include mandatory accreditation of testing laboratories to ensure quality pesticides reach farmers, and provisions for compounding of offences with enhanced penalties to be defined by State-level authorities.

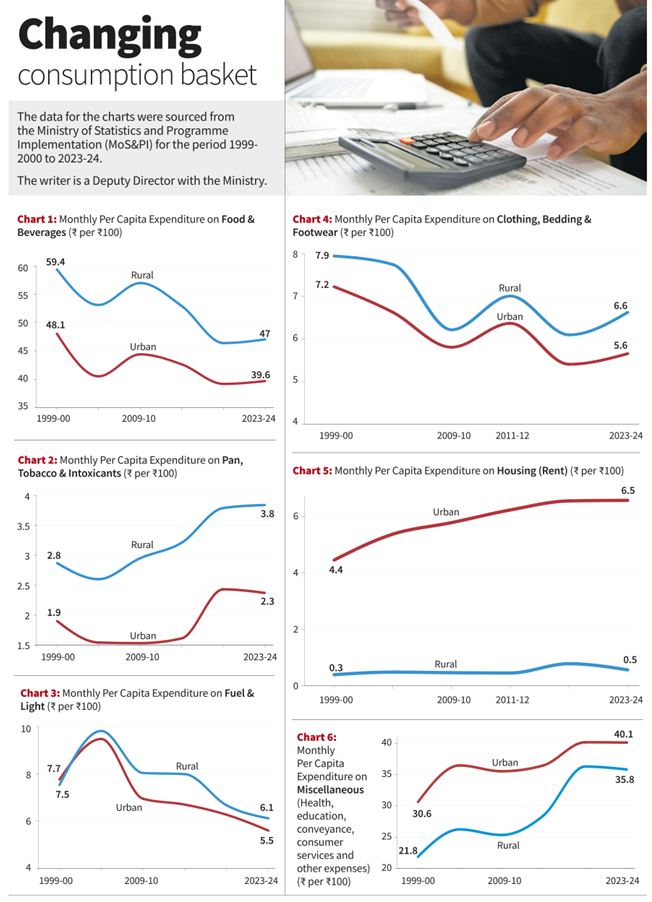

Context: Indians are shifting from subsistence needs to aspirational and service-oriented spending.

The Household Consumption Expenditure Survey (HCES) by the Ministry of Statistics and Programme Implementation (MoS&PI) captures spending pattern of Indian households across various consumption categories.

Conducted every five years, the HCES provides granular estimates of Monthly Per Capita Expenditure (MPCE) for both rural and urban populations, covering a wide range of goods and services.

The survey rounds for 2022-23 and 2023-24 represent the first comprehensive update to MPCE data in over a decade, offering valuable insights into India’s shifting consumption landscape. These findings are central to revising poverty estimates, informing social sector policy, and understanding the lived realities of India’s expanding middle-income population.

This article examines long-term MPCE trends from 1999-2000 to 2023-24, with a focus on six key expenditure categories. In this analysis, MPCE is expressed as the proportional expenditure on an item for every ₹100 of total spending.

Decline in MPCE share on food and beverages for both urban (from ₹48 to ₹39 per ₹100) and rural areas (from ₹59 to ₹47 per ₹100) confirms Engel’s Law, which states that as real income rises, the proportion of income spent on food declines, even if absolute expenditure increases. (Chart 1)

Further, a fall in expenditure on cereals, alongside higher spending on fruits, eggs, fish, and processed foods, signals a shift from staple-heavy diets to more varied, protein-rich diets — albeit unequally.

Despite marginal increases, particularly in rural areas, spending on pan, tobacco, and other intoxicants remains a low share of MPCE, accounting for under ₹3.8 per ₹100 of spending. From a public health perspective, the trend calls for targeted awareness programs in rural belts. (Chart 2)

The reduction in per capita fuel spending reflects policy successes, such as Saubhagya (rural electrification) and PM Ujjwala Yojana (LPG access). Lower urban spending may also reflect the use of energy-efficient appliances and access to reliable power supply. Modern fuels, in place of biomass or kerosene, improve quality of life and are an example of expenditure substitution. (Chart 3)

The decline in spending on clothing, bedding and footwear is moderate and consistent with the transition from need-based consumption to periodic discretionary spending. Rising competition, fast fashion, and lower textile prices may also have contributed. Rural India’s slightly higher or similar spending may indicate seasonal dependence and growing aspirations. (Chart 4)

The urban housing rent share rose significantly (₹4.46 to ₹6.58 per ₹100), aligning with urbanisation, rental stress, and migration to metropolitan hubs. Rural rent remains minimal due to widespread self-owned housing, informal tenure, or rent-free arrangements. (Chart 5)

The miscellaneous category includes aspirational expenses such as health, education, conveyance, consumer services, and other similar costs. Its rising share, particularly in rural MPCE (from ₹21.87 to ₹35.82 per ₹100), reflects a broadening of the consumption basket. This trend aligns with inclusive growth, deeper digital penetration, and echoes improved reach and quality of both public and market-based services. (Chart 6)

Taken together, these trends reflect that society is undergoing an economic transition, with consumption patterns gradually shifting away from subsistence needs toward more aspirational and service-oriented spending.

Context: The Indian Space Research Organisation (ISRO) is scheduled to launch the PSLV-C62/EOS-N1 Mission on January 12.

Strategic use

The launch of the earth observation satellite (EOS-N1) satellite along with other payloads will take place from the first launch pad of the Satish Dhawan Space Centre at Sriharikota in Andhra Pradesh.

EOS-N1 is an earth imaging satellite said to be built for strategic purposes. ISRO has not shared further details about the satellite. “The launch of PSLV-C62 Mission is scheduled on 12 January 2026 at 10:17 hrs IST,” ISRO posted on X.

The PSLV-C62/EOS-N1 mission is the first launch for ISRO in 2026 and comes within a few days of successfully launching the U.S.’s BlueBird Block-2 satellite communication satellite in low earth orbit on December 24 onboard the LVM-3 launch vehicle.

Post glitch

The launch of the PSLV-C62/EOS-N1 mission will be the 105th launch from Sriharikota.

It is also an important launch for the space agency as the Polar Satellite Launch Vehicles (PSLV), which is ISRO’s workhorse, had suffered a glitch during its previous attempt to launch a satellite.

On May 18, 2025, while ISRO attempted to launch the EOS-09 satellite aboard the PSLV-C61 it could not accomplish the mission due to an observation in the third stage of the rocket.

PSLV-C62/EOS-N1 Mission will also launch payloads developed by start-up and academia from India and abroad.

Context: Higher estimate comes amid uncertainties and 50% U.S. tariffs hitting labour-intensive sectors hard; with Q1 and Q2 growing at 7.8% and 8.2%, second half will see average growth slow to 6.8%.

The Union government has estimated that real growth in the Gross Domestic Product (GDP) of the country will stand at 7.4% in the current financial year 2025-26, up from 6.5% recorded the previous year.

In the First Advance Estimates (FAE) of GDP for 2025-26, released by the Ministry of Statistics and Programme Implementation, the government said that nominal growth for the year would be 8%.

The FAE for any year is important as it forms the basis for various calculations and ratios used in preparing the Union Budget.

The First Advance Estimates, and the Second Advance Estimates, which will be released on February 27, are forecasts of the full year’s growth based on data available up to that point. The Provisional Estimates for 2025-26, based on the full-year’s data, will be released on May 30.

Based on the Centre’s assessment that the full year’s growth would be 7.4%, and the fact that Q1 and Q2 saw 7.8% and 8.2% growth respectively, the second half of the year would see average growth slow to 6.8%.

Braving headwinds

In December, the Reserve Bank of India had said that GDP growth in 2025-26 would be 7.3%, with Q3 growing at 7% and Q4 at 6.5%.

These projections come at a time when India’s economy is facing several headwinds. The 50% tariff levied by the U.S. on imports from India has hit several labour-intensive sectors such as apparel, textiles, and engineering goods.

The government has tried to boost consumer demand through both direct tax and indirect tax rate cuts, but the data show it nevertheless expects Private Final Consumption Expenditure, a metric that captures consumer spending, to grow at 7% in 2025-26, marginally slower than the 7.2% recorded last year.

The mining and quarrying sector is estimated to contract in 2025-26 by 0.7%, as compared to a growth of 2.7% the previous year.

The tertiary sector, which comprises the service sectors, is expected to see growth quicken to 9.1% in 2025-26 from 7.2% in 2024-25. Within this, the ‘financial, real estate and profession services’, and the ‘public administration, defence, and other services’ sub-groupings are both expected to grow at 9.9% in 2025-26.

The ‘trade, hotels, transport and communication’ category is expected to grow at a relatively slower 7.5% in 2025-26, although this is faster than the 6.1% seen in 2024-25.

Gross Fixed Capital Formation, on the other hand, is expected to grow at 7.8% in 2025-26, faster than the 7.1% seen in 2024-25.

ಸಂದರ್ಭ: ಉಕ್ರೇನ್ ಮತ್ತು ರಷ್ಯಾ ನಡುವೆ ಸಮರ ಆರಂಭವಾದ ನಂತರದಲ್ಲಿ ಭಾರತವು ರಷ್ಯಾದಿಂದ ಅಂದಾಜು 144 ಬಿಲಿಯನ್ ಯೂರೊ (ಸರಿಸುಮಾರು ₹15.19 ಲಕ್ಷ ಕೋಟಿ) ಮೌಲ್ಯದ ಕಚ್ಚಾ ತೈಲವನ್ನು ಆಮದು ಮಾಡಿಕೊಂಡಿದೆ ಎಂದು ಯುರೋಪಿನ ‘ಇಂಧನ ಮತ್ತು ಶುದ್ಧ ಗಾಳಿ ಕುರಿತ ಸಂಶೋಧನಾ ಕೇಂದ್ರ’ (ಸಿಆರ್ಇಎ) ಅಂದಾಜು ಮಾಡಿದೆ. ಇದೇ ಅವಧಿಯಲ್ಲಿ ಚೀನಾ ದೇಶವು ರಷ್ಯಾದಿಂದ ಅಂದಾಜು 210 ಬಿಲಿಯನ್ ಯೂರೊ ಮೌಲ್ಯದ (ಸರಿಸುಮಾರು ₹22.16 ಲಕ್ಷ ಕೋಟಿ) ಕಚ್ಚಾ ತೈಲವನ್ನು ಖರೀದಿಸಿದೆ. ಭಾರತವು ರಷ್ಯಾದಿಂದ ಕಚ್ಚಾ ತೈಲ ಮಾತ್ರವೇ ಅಲ್ಲದೆ 18.18 ಬಿಲಿಯನ್ ಯೂರೊ (ಸರಿಸುಮಾರು ₹1.91 ಲಕ್ಷ ಕೋಟಿ) ಮೌಲ್ಯದ ಕಲ್ಲಿದ್ದಲನ್ನು ಕೂಡ ಖರೀದಿಸಿದೆ. ಚೀನಾ ಕೂಡ ರಷ್ಯಾದಿಂದ ಹಾಗೂ ಅನಿಲವನ್ನು ಕಲ್ಲಿದ್ದಲು ಖರೀದಿಸಿದೆ. ಇದೇ ಅವಧಿಯಲ್ಲಿ ಐರೋಪ್ಯ ಒಕ್ಕೂಟವು ರಷ್ಯಾದಿಂದ ಒಟ್ಟು 218.1 ಬಿಲಿಯನ್ ಯೂರೊ (ಸರಿಸುಮಾರು ₹23.02 ಲಕ್ಷ ಕೋಟಿ) ಮೌಲ್ಯದ ಪಳೆಯುಳಿಕೆ ಇಂಧನವನ್ನು (ಕಲ್ಲಿದ್ದಲು. ತೈಲ ಮತ್ತು ಅನಿಲ) ಖರೀದಿಸಿದೆ.

ಸಂದರ್ಭ: ದಿವಂಗತ ಮೈಸೂರು ಅನಂತಸ್ವಾಮಿ ಸಂಯೋಜಿಸಿದ ಧಾಟಿಯಲ್ಲಿ’ಜಯ ಭಾರತ ಜನನಿಯ ತನುಜಾತೆ…’ ನಾಡಗೀತೆ ಹಾಡುವ ಸಂಬಂಧ ರಾಜ್ಯ ಸರ್ಕಾರ ಹೊರಡಿಸಿದ್ದ ಆದೇಶವನ್ನು ಪ್ರಶ್ನಿಸಿ ಗಾಯಕ ಕಿಕ್ಕೇರಿಕೃಷ್ಣಮೂರ್ತಿಸಲ್ಲಿಸಿದ್ದ ಮೇಲ್ಮನವಿಯನ್ನು ಹೈಕೋರ್ಟ್ ವಜಾಗೊಳಿಸಿದೆ.

‘ನಾಡಗೀತೆಗೆ ಮೈಸೂರು ಅನಂತಸ್ವಾಮಿ ಅವರ ಧಾಟಿಯನ್ನು ಅಳವಡಿಸಿಕೊಂಡು ಅದರ ಪೂರ್ಣಪಾಠ ಬಳಸಬೇಕು ಹಾಗೂ ಅಲಾಪವಿಲ್ಲದೇ, ಪುನರಾವರ್ತನೆ ಇಲ್ಲದೆ 2 ನಿಮಿಷ 30 ಸೆಕೆಂಡುಗಳಲ್ಲಿ ಹಾಡಬೇಕು’ ಎಂದು ರಾಜ್ಯ ಸರ್ಕಾರ ಹೊರಡಿಸಿದ್ದ ಆದೇಶವನ್ನು ಪ್ರಶ್ನಿಸಿ ಕಿಕ್ಕೇರಿ ಕೃಷ್ಣಮೂರ್ತಿ ಹೈಕೋರ್ಟ್ ಮೆಟ್ಟಿಲೇರಿದ್ದರು.

Context: India’s solar module manufacturing has increased to more than twice since last year, Union Minister for New and Renewable Energy. Solar module manufacturing has increased 128.6% on a year-over-year basis to 144 gigawatts (GW) in 2025. It stood at 63 GW in 2024. This implies that India added 81 GW-worth of capacity in the previous year.

Government initiatives such as PM-Surya Ghar, solar parks, and international collaborations through the International Solar Alliance (ISA) have positioned India as the third-largest solar power producer worldwide.

🌞 Solar Energy in India: Growth, Achievements, and Future Pathways 📌 Current Status Installed Capacity: India’s solar installed capacity crossed 130 GW in November 2025, up from 94 GW in 2024, marking a 41% growth in one year.

Manufacturing Expansion: Solar module manufacturing more than doubled in 2025, rising from 63 GW in 2024 to 144 GW in 2025, a 128.6% increase.

Global Ranking: India overtook Germany in 2024 to become the third-largest generator of wind and solar power, producing over 108,494 GWh of solar electricity, surpassing Japan.

🏛️ Government Initiatives PM-Surya Ghar: Over 8.5 lakh rooftop installations completed by January 2025, aiming to power 10 million households with solar energy.

Solar Parks & Ultra-Mega Projects: Over 3 GW commissioned in 2025 under the Solar Parks scheme.

International Solar Alliance (ISA): India hosted the 8th ISA Assembly in October 2025, strengthening global cooperation on solar technology and finance.

Policy Push: India achieved 100 GW solar capacity milestone in February 2025, five years ahead of its COP26 commitment.

📊 Key Achievements: India’s Solar Capacity

Year

Installed Solar Capacity

Milestone

2014

~9 GW

Early stage

2024

94 GW

Rapid growth

2025

130 GW

41% YoY growth

2025

144 GW (manufacturing)

Doubling of module capacity

2030 (Target)

500 GW (non-fossil)

COP26 commitment

☀️ India’s Solar Energy: Current Status (Jan 2026) India achieved a major milestone in 2025 by reaching 50% non-fossil fuel capacity five years ahead of the 2030 target.

Metric

Capacity / Achievement (as of Dec 2025/Jan 2026)

Cumulative Solar Capacity

132.85 GW (Crossed 100 GW mark in Jan 2025)

Total Non-Fossil Capacity

263 GW (Includes Solar, Wind, Hydro, and Nuclear)

Annual Addition (2025)

~35 GW (Solar alone; record-breaking year)

Global Ranking

3rd Largest solar producer (surpassing Japan in 2025)

Largest Solar State

Rajasthan (~36 GW), followed by Gujarat and Maharashtra

🏭 Solar Manufacturing & Industry Growth Through the Production Linked Incentive (PLI) scheme, India has moved from an importer to a dominant manufacturer.

Manufacturing Category

Annual Capacity (Jan 2026)

2024 Comparison

Solar PV Modules

144 GW

128.6% increase from 63 GW in 2024

Solar Cells

24 GW

Rapidly scaling under ALMM List-II

Solar Wafers

~5.3 GW

Target of 50 GW+ by 2028

Top State for Mfg

Gujarat

Accounts for 41.6% of module production

🏠 Major Solar Schemes & Implementation

Scheme

Target

Current Achievement (Jan 2026)

PM Surya Ghar

1 Crore (10 Million) Homes

2.4 Million households solarized; 7 GW added.

PM-KUSUM

34.8 GW (Solar for Farmers)

10.2 GW installed; 20 Lakh+ solar pumps.

Solar Parks

40 GW Approved

55 Solar Parks sanctioned across 13 states.

🎯 Roadmap to 2030 (The “Panchamrit” Goal)

Target Year

Milestone

2026-27

Target of 1 Crore households under PM Surya Ghar.

2030

500 GW of non-fossil fuel capacity (Solar to be ~280-300 GW).

2070

Net Zero Emissions for the nation.

🌍 Significance Energy Security: Solar is India’s most secure energy source, abundantly available across regions.

Climate Goals: India achieved 50% renewable share of total installed capacity (484 GW) by 2025, five years ahead of target.

Economic Impact: Expansion of solar manufacturing reduces import dependence, creates jobs, and boosts domestic industry.

Global Leadership: India is now a founding leader of ISA, influencing solar deployment across 125+ nations.

⚠️ Challenges Ahead Land Acquisition: Large-scale solar parks face land hurdles, prompting PSUs to form joint ventures with states.

Grid Integration: Need for stronger payment security and wholesale market reforms to integrate solar efficiently.

Storage & Transmission: Scaling battery storage and transmission infrastructure is critical for balancing intermittent solar supply.

✨ Conclusion India’s solar journey reflects a bold leap toward a net-zero future, with achievements like 100 GW solar capacity, 144 GW manufacturing, and global leadership through ISA. While challenges in land, grid integration, and rooftop adoption remain, India’s trajectory shows it is well on course to meet its 500 GW renewable energy target by 2030 and long-term vision of 1,800 GW green energy by 2047.

Context: As the scheme, in its third year now, is production-linked, higher output levels necessitate a corresponding scale-up in incentives.

The Ministry of Heavy Industries (MHI) has proposed doubling the allocation for the Production Linked Incentive (PLI) scheme for automobiles and auto component manufacturers to ₹5,800 crore in the upcoming financial year. The scheme had received ₹2,818.85 crore in FY 2025-2026.

The PLI auto scheme incentivises local production of only those products that achieve a domestic value add (DVA) of 50%. The scheme was focused on zero emission vehicles (ZEVs), i.e., battery electric vehicles and hydrogen fuel cell vehicles.

The scheme was announced in 2021, but FY 2023-24 was the first performance year, and an amount of ₹322 crore was disbursed to four approved applicants in FY 2024-25. For the performance year 2024-25, a total amount of ₹1,999.94 crore was disbursed for five approved applicants.

Looking ahead, the target allocation for FY 2027-28 is nearly ₹8,000 crore, increasing to ₹9,500 crore in the fifth year.

These allocations are aimed at achieving the total outlay of ₹25,938 crore as defined when the scheme was launched in 2021.

Explaining the rationale behind seeking doubling of allocation, that in the initial years, the OEMs were focused on setting up manufacturing plants, which required substantial capital investment. Now, in the third year of the scheme, the focus would be on ramping up production output. As the scheme is production-linked, higher output levels necessitate a corresponding scale-up in incentives.

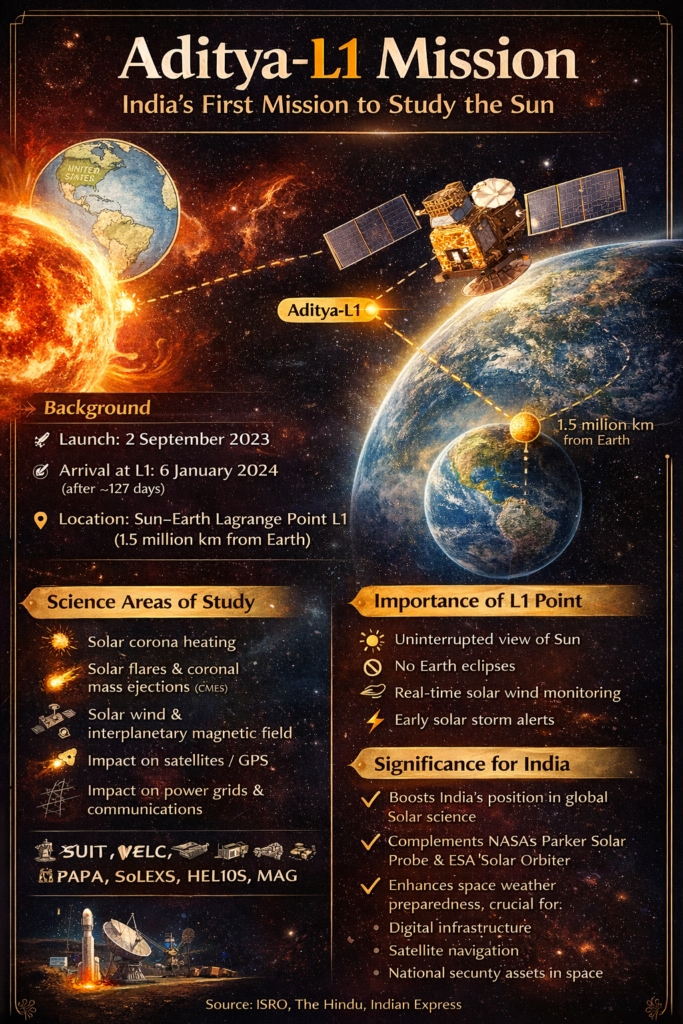

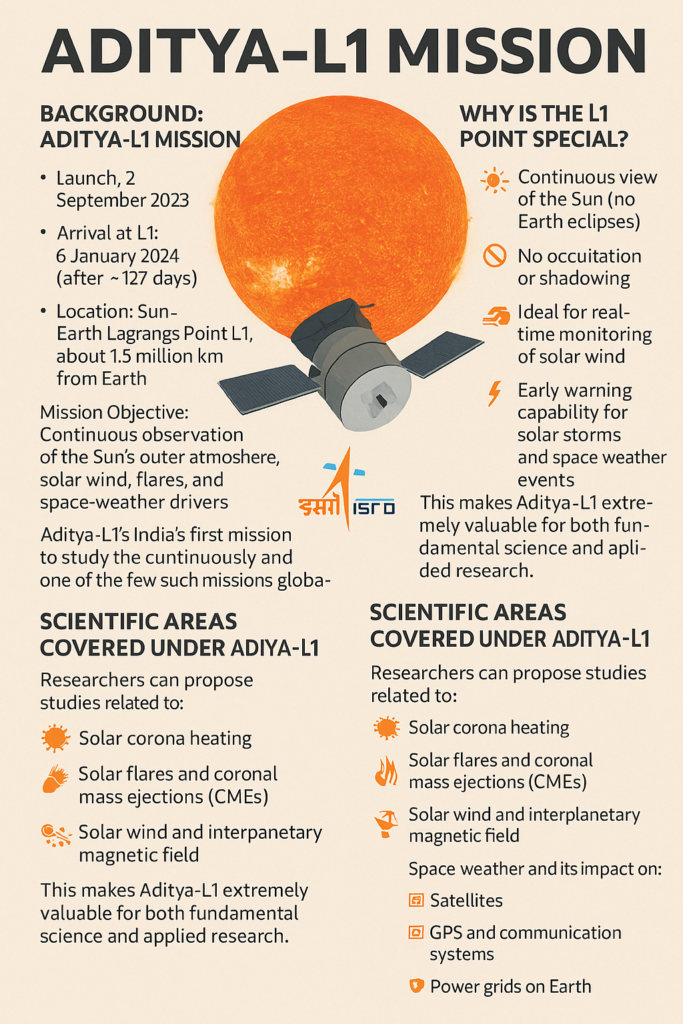

Context: On the second anniversary of India’s maiden solar mission Aditya-L1 reaching the Lagrangian point (L1), the Indian Space Research Organisation (ISRO) made the Announcement of Opportunity (AO) soliciting proposals for the first AO cycle observations.

The Aditya-L1 spacecraft reached the L1 point on January 6, 2024, 127 days after it was launched on September 2, 2023, and since then has been making continuous and comprehensive observations of the Sun from the Sun–Earth L1 point.

According to ISRO, scientific data from the mission are regularly released in public domain for global scientific utilisation.

To maximise return

“At present there are more than 23 TB data in public domain and several important scientific results have been published in International peer reviewed journals. To further maximise the scientific return from this unique mission, the ISRO has released the first AO inviting proposals from the Indian solar physics community for Aditya-L1 observation time,” ISRO said.

It added that this L1 point, located approximately 1.5 million kilometers away from Earth, offers the unique advantage of continuous, uninterrupted observation of the Sun, free from eclipses or occultation.